LOGISTIC Sector Analysis FY22-23. 3PL, Smart warehousing, the new Bahubalis of the Indian Logistic sector.

In the below picture, you might remember a scene from the legendary comedy movie “Hangover.” In the scene, three friends and the groom(Doug) are getting ready for Doug’s marriage on their way back from Las Vegas Bachelor Party. With Doug’s wedding set to occur in five hours, they ordered Wedding dresses from a shop, and the delivery was done on the road at high speed with no time to waste for a stop and to get ready. Finally, they are ready, and they join the wedding. This is the modern-day Logistic scenario; speed is the need. Customers are expecting faster deliveries day by day.

With the Pandemic hit, the Logistic sector was one of the most affected sectors in India. Both topline and bottom-line growth declined. Supply chains were disrupted. The GDP of the country declined drastically. But do you wonder what the current scenario of today’s Logistics companies is? Did it recover to the pre-Covid level? If yes, what are the investment opportunities? Will the Ukraine war, which continued the supply chain disruption, affect growth in Indian Logistic companies? Before investing in it, you must first understand the sector and business niche of the companies.

In the last Decade of the Indian economy, E-commerce was the apple of the Investor’s eye. Many big players transformed the e-commerce sector to a different level. But along with that, one sector that showed a paradigm shift in demand was Logistic Sector. There was a high growth in the Market capitalisation of Logistic stocks, whether a Road express stock or third-party (3PL) logistic-providing company stock. Currently, the Logistic cost of India’s GDP is about 14%. The Government of India is trying to reduce that to 8% by implementing various policies through National Logistic Policy. Developed countries like the USA have a logistic cost of 8% of GDP, and In China, it is around 9% of GDP. To achieve a goal of 8% of the GDP cost of logistics, India has to build good transportation infrastructure, smart warehouses, and many more. This brings a humongous opportunity for the Logistic sector to grow more.

It would be hard to imagine a day without logistics in the modern-day world. With changing political situations, economic crises, and various global uncertainties, it is essential for an investor to know the present-day opportunities a logistics sector company possesses. With the use of technologies and AI, we can see many smart warehouses and digitalized-robotized parcel delivery processes in the coming days. Present-day companies have started using many data-driven forecasting models to improve logistic management and cost. Achieving a 5 trillion USD economy is only possible by enhancing the growth engine Logistic Industry.

In this article, first, we will try to understand what a logistic sector is, how it is performing, what growth aspects are, what challenges it still has, and the investment opportunity in this sector.

Understanding the logistics Sector

Although warfare and military practices from history showed the use of logistic management, the birth of the Industrial era in the mid-19th and 20th centuries led to considerable change in this sector. Technological innovation, machines, and communication transformed the sector to a whole new level. The IT, automation, and use of data analytics in the logistic sector has improved the supply chain management process in the modern day. Supply chain management takes care of the flow of goods and services, with Logistics being a vital part of the system. Today from the source of raw material to production, and delivery of the same to customers consists of various logistic management processes.

The logistics sector can be classified into three significant Categories in India -Roads, Rail, Air, and Cross border logistics. 60%-70% of the Logistic Market belongs to Roads, which consist of Full Trucking and Partial Trucking transportation. Currently, the Indian Logistic market is pegged at 250Bn USD, expected to grow to 380Bn dollars in FY25 at a CAGR of 10-12% growth. In Rail transport, the Container Corporation of India(CONCOR) has the monopoly of being a single player in the sector. Similarly, Allcargo, Gateway Distrparks has the business advantage of being a significant leader in cross-border logistics.

Logistics can also be classified into Transportation, distribution, and Storage. Storage or warehousing is indispensable in any business's supply chain. Warehouses are the parts where the Goods are stored before they are dispatched.

Growth Aspect of the Logistic Sector

The market size is expected to grow to 380Bn USD in India by FY-25. Even with the Pandemic hit and Russia-Ukrain war tensions, the Indian Logistics market has recovered well because of the solid intrinsic demand of India's huge population. There has been an increase in demand from tier 2 and tier 3 cities in India in the last few years. The overall logistic cost of India can be achieved on par with the USA only by making better transportation and reducing the wastages and inefficiencies(which constitute 4.3% of GDP). Scenarios are changing now; the warehousings are being digitalized and robotized for better efficiency. The multi-modal seamless connectivity infrastructures are being developed by Government’s Gati Shakti Yojana.

Earlier, rail transport was the dominant mode of transport, but in the last seven years, the mode of transport has shifted more towards Road. This massive shift of transport from rail (80% to 31%) to road brings the most enormous opportunity for Full truckload(FTL), Part truckload(PTL), and Road express companies like Blue dart, TCI Express, VRL logistics, Delhivery, etc.

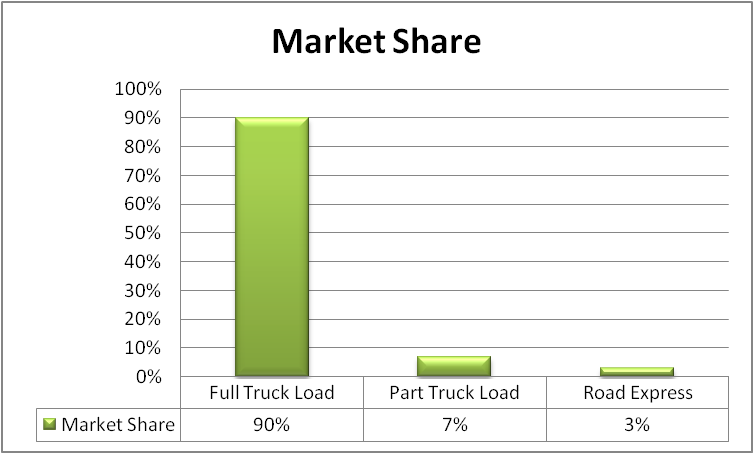

Full Truck Load has the highest market capture, then the Part truck Load and Road express. In FTL, the trucks are fully occupied with Goods, and in Part truckload, the trucks are semi-occupied.

With Government’s new policies, and GST implementation, the establishment of Logistic Parks has been a primary driver in the Warehousing sector. The 3PL(Third Party Logistics) companies are on a bull ride now and are expected to continue the trend in the Future. The unprecedented rise of the E-commerce industry is the cause of the third-party logistic industry growth. Now Companies are hiring a third party to take care of their supply chain activity, from packaging to transportation. Most e-commerce companies are outsourcing their non-core business operations to these 3PL companies. Auto component-producing companies are also some big customers of these 3PL companies. Allcago Logistics and Mahindra Logistics are vital players in the trending 3PL industry.

Initially, India Post started Express parcel delivery in India, and some foreign players had market control, like DHL, FedEx, TNT, UPS, etc. TCI Express and Bluedart took the Indian express industry forward as domestic players. As per customers' usage, the express industry can be classified into B2B and B2C segments. With the growth of e-commerce, the B2C market surpassed the B2B market size in a decade. The B2C market is supposed to grow at a CAGR of 25% to USD 100Bn by 2025, and so will the B2C logistics.

Blue dart Express has that business niche of being a dominant player in delivering business-to-business Air cargo delivery. The air cargo B2B is very time-sensitive. Rail delivery in express logistics has declined over the year and is rarely used. That’s why CONCOR(Container Corporation of India) has shown stagnant growth numbers in sales and PAT in recent years.

In the future, companies showing an inclination toward data analytics, warehousing automation, blockchain, first mile, and last mile automation should show a faster growth rate.

Challenges for the Logistic sector

The cons and challenges in India are the poor infrastructure of Roads, increasing price of trucks, pilferage, damage, and wastage are still a headache in this sector. The Logistic market is becoming highly competitive. There is much room for development in India in technology and infrastructure. The industry is very Asset heavy, so reducing overhead costs becomes very important.

Talking about overheads, a start-up company Rivigo has done a marvellous job of reducing it. They have developed the Relay trucking model. This means” The driver is changed at every certain distance, and the truck never stops.” This has brought down the transit time. Rivigo has been taken over by Mahindra Logistics this year. The transit speed has increased from 30 km/hr to 45 km/hr, reducing costs.

Investment Opportunity

While investing, it is essential to look at numbers. Delhivery Ltd, like start-up companies, is expanding business aggressively, but on the other hand, they may not fetch you good returns now as their expenditure is too high on expansion. CONCOR, although it has the monopoly in Rail express, the growth numbers in top line and bottom line almost flat. Now, if we filter out stocks having some business advantage, Market leaders, as per their Market capitalisation, with a Debt to Equity ratio of lesser than 1.5 times and a ROCE of greater than 15%, we got some of the below few logistics companies found to be investment worthy.

Allcargo Logistics

Allcargo, led by acquisitions, is present in more than 90 countries. It is a significant player in cross-border logistics. It is also a leading player in 3PL logistics in India. Recently it also acquired Gati, like leading express delivery company. The company's valuation seems interesting, with a PE multiple of 10.94 and a ROCE of almost 26.41. Over the last five years, revenue has grown at a yearly rate of 29.22%, vs an industry avg of 9.12%, and the profit grew at a CAGR of 31.60%.

Aegis Logistics

This company has astonishingly managed to reduce its overhead costs. It has the business advantage of being the leading player in India’s Oil, Gas, and Chemical sector. The LPG transport business is supposed to grow in the coming years as the demand for energy in India is increasing. The company's major clients are BPCL, HPCL, Reliance Industries, Caltex, Supreme Industries, etc. With leading industrial clients, the company has shown a growth of 20.49% YOY from the previous year in topline revenue. The company is expanding into new markets too internationally.

Transport Corporation of India

Transport Corporation Of India is a leader in integrated multimodal Logistic company. Over the last five years, revenue has grown at a yearly rate of 10.9%, vs the industry avg of 9.12%. However, there was an impressive growth of 29% CAGR in profit in the last five years. The company is debtless.

This was a brief analysis of the Logistic sector and supply chain companies. We see positive long-term growth in this sector, with growing demand due to various factors we discussed.

Key takeaways

- 3PL Providing companies will grow at a faster rate.

- Road transport companies will always have more business opportunities.

- The traditional way of handling Logistics companies will fade away if they become incompetent with technology-focused innovative logistics companies.

Article Source

https://www.wisbees.com/logistic-sector-analysis-fy22-23-3pl-smart-warehousing-the-new-bahubalis-of-the-indian-logistic-sector/

https://www.wisbees.com/logistic-sector-analysis-fy22-23-3pl-smart-warehousing-the-new-bahubalis-of-the-indian-logistic-sector/

https://www.wisbees.com/logistic-sector-analysis-fy22-23-3pl-smart-warehousing-the-new-bahubalis-of-the-indian-logistic-sector/

https://www.wisbees.com/logistic-sector-analysis-fy22-23-3pl-smart-warehousing-the-new-bahubalis-of-the-indian-logistic-sector/

https://www.wisbees.com/logistic-sector-analysis-fy22-23-3pl-smart-warehousing-the-new-bahubalis-of-the-indian-logistic-sector/