Flexi Cap! But which one...

Modern Problems require Modern Portfolios

Imagine you are a modern day Cristopher Columbus, you want to cross the ocean to visit a far off land in search of gold that people can only dare to dream of, would you rather take a battleship, a cruise ship or a speed boat to get to your destination ? Of course, you would prefer a battleship when the waters are stormy, a cruise ship when you want to move slightly faster with lesser stability and a speed boat when you want to get there faster. Sometimes you would even need a life raft when things are going south. The same idea works for mutual funds; you need different types of funds to cross different types of obstacles. Now imagine if you could switch between these vessels when and where you want, at a tip of the hat! Mr. Columbus didn’t have that luxury, but you do, at least when it comes to the stock market.

Ever since it came into existence, flexi caps have been a rage in the Indian market and why shouldn’t they be? They allow you to seamlessly change between market caps (ships in the above example) whenever you want. These funds are run by expert fund managers (captain of these ships) and they along with their team (the crews on these ships) gauge the weather before choosing which ship to take.

- Flexi Cap funds allow managers to dynamically invest across large, mid, and small caps with a minimum 65% equity allocation.

- PPFAS Flexi Cap follows a highly diversified, globally exposed strategy with hedged equity and debt components.

- HDFC Flexi Cap takes a more concentrated, conservative approach with strong large-cap orientation.

- Both funds have consistently outperformed the NIFTY 500 TRI across 3, 5, and 10-year horizons.

- PPFAS manages a larger AUM, while HDFC offers relatively greater flexibility due to lower scale.

- Both schemes are suited for long-term investors with a minimum 7-year investment horizon.

A brief introduction on Flexi Caps

Flexi cap funds were formally introduced in India on November 6th, 2020, by SEBI. The minimum investment in equity and equity-related instruments was set at 65% of the total investment assets. The fund managers have the freedom to invest across any market capitalization, large, mid or small. As per SEBI, any existing scheme can be converted to a flexi cap scheme, provided it follows the required attributes. The need for flexi-cap schemes arose when multi-cap schemes were restricted by SEBI to invest at least 75% of their total assets in equity and equity-related securities, with a minimum 25% exposure to each cap. SEBI was forced to impose these restrictions because most multi- cap funds had turned their focus purely towards the large caps. This raised concerns among the investors who were looking for a good mix of stocks across market caps. SEBI’s intervention created a distinction between these two schemes.

Flexi-cap schemes allow the fund manager to move across the market caps as and when they deem fit; they are no longer restricted to a particular capitalization where they no longer see any value. This can naturally create alpha as the fund houses do not have their hands tied. The job of a flexi cap fund manager is the toughest, as they have to constantly look ahead into the future while making decisions in the present.

Let’s talk about two of the best flexi-cap schemes in the market today, Parag Parikh Flexi Cap and HDFC Flexi Cap. Through this article, we will know about their backgrounds and how they are performing today across all these years of changing macros.

I will start by introducing these funds and their fund houses to you.

Parag Parikh Flexi Cap

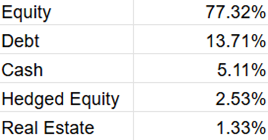

Parag Parikh Flexi Cap is the flagship fund of its fund house, PPFAS Mutual Fund. The fund was officially launched on 10th October 2012. Initially, it was named “Parag Parikh Long Term Equity Fund”. It was renamed and reclassified as a Flexi Cap fund following the 2020 regulatory change. In a market where the fund managers change every few years, the scheme has shown exceptional stability in its core management team since inception, with Mr. Rajeev Thakkar as its Chief Investment Officer and lead fund manager from day one. It follows the philosophy of a Swiss army knife, unlike most of its peers; PPFAS Flexi Cap is known to invest in the international market as well. They look for companies with low debt, high cash flows, and investor-friendly management. They make sure that not only is the company good, but also that it is trading below its fair value. The fund has consistently outperformed its benchmark – NIFTY 500 TRI in the 3, 5 and 10-year horizons. The AUM is the highest in the industry at ₹1,33,969.81 Cr with an expense ratio of 0.63%. The fund house ranks 23rd in total assets with ₹1,51,899.28 cr., the flexi cap scheme forming most of it (approx. 88%).

HDFC Flexi Cap Fund

The HDFC Flexi Cap fund is the go-to fund for people who feel PPFAS Flexi is too saturated. Starting from January 1, 1995, this fund was formally known as the HDFC Equity Fund and later became the flexi-cap we know of. HDFC Mutual Funds is one of the most reputed fund houses in the country, and it ranks 2nd in total assets under management. The team managing the scheme is slightly volatile when compared to PPFAS, with Mr. Prashant Jain at the helm for 19 years, followed by Ms. Roshi Jain, and most recently, starting from 1st Feb 2026, Mr. Amit Ganatra. Naturally, each CIO has a different approach when it comes to their investment philosophy. Investors should make a note of this before choosing. The scheme currently has an AUM of ₹97,451.56 cr and lags more than ₹30,000 cr behind PPFAS. The lower AUM does not prove its poor performance in any way as it too has beaten the index (Nifty 500 TRI) by considerable margins in the 3-, 5-and 10-year periods. It charges a barely higher expense ratio at 0.69%.

Holding Structure Analysis

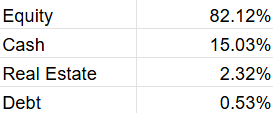

Let us compare the holdings of both the funds and understand where their concentration lies.

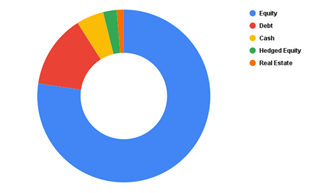

PPFAS Flexi Cap

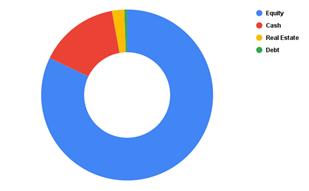

HDFC Flexi Cap

Right from the onset we can see that HDFC is heavier on equity, cash and real estate by sacrificing its debt holdings. PPFAS seems to be much more diversified by holding less equity, cash and real estate, it has significantly more debt holdings and a portion of its AUM allocated to hedged equity.

Here’s a deeper dive at their holdings:

PPFAS Flexi Cap -

- Total holdings - 221

- Funds allocated to equity - ₹1,03,585 Cr

- A breakdown of equity holdings include - Financial (33.8%), Technology (25.29%), Consumer Discretionary (12.54%), Energy & Utilities (8.01%), Consumer Staples (7.48%), Materials (7.46%), Healthcare (5.21%) and Industrials (.2%).

- Holdings are highly diversified with domestic and foreign equities, REITs, certificate of deposits, commercial papers, T-Bills, Partly Paid Equity shares, futures, call options and a tiny amount (.45%) in its own liquid fund.

- As of Feb 13, 2026 it maintains a predominantly large cap portfolio with very small exposures mid and small caps, with approximately 72% of its total holdings in large cap.

HDFC Flexi Cap -

- Total holdings - 55

- Funds allocated to equity - ₹80,027 cr

- A breakdown of equity holdings include - Financial (47.10%), Consumer Discretionary (16.87%), Technology (11.20%), Healthcare (8.18%), Materials (6.61%), Energy & Utilities (4.77%), Industrials (4.29%) and Consumer Staples (0.97%).

- HDFCs holdings are a lot less diversified and show a more conservative approach. They include equity, REITs and Government Securities only.

- As of Feb 13, 2026, it too maintains a predominantly large cap portfolio with approximately 70% of its AUM in it.

We can observe that both funds are deeply invested in Large Cap companies. Large Caps are like huge ships, during a storm they can bear the brunt and violence of storms and keep afloat. If the weather forecast tells you there is a storm ahead, would you rather choose a battleship with an experienced captain or a dingy? I believe the same goes for these flexi cap fund managers who are captains on their own rights.

Everybody dreams of riding the storm, but have you got the guts for it?

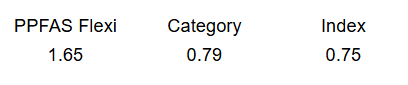

Not all risks are worth taking, because if that were true, every gambler would have been a billionaire. At the stock market every decision comes at a cost and you need to decide whether these schemes are worth the risk they take before you invest. The Sharpe ratio is a tool that can help you take that decision. The higher the ratio is, the better the fund is at managing risks, the basic criteria for your fund of choice should be to beat the index first and then its category average (avg of all flexi schemes). Since, both these funds have already done that, let’s see where they stand among themselves.

PPFAS Flexi

HDFC Flexi

As we can see, both beat their categories and the index by quite a margin. PPFAS fairs slightly better than HDFC though. They have both made greater returns than the amount of risk they undertook.

Enough about the risks, let’s talk about the rewards

Both these funds are at the top of their games. They beat their index and their category average in terms of returns, but where do they stand among themselves? It is said that past returns are not an indicator of future performances, but I believe they can say something about the direction things might go if similar situations prevail. An example can be about a fund manager’s reaction to a macroeconomic event; someone may time it wrong but get it right along the way. These small delays can cost fund managers percentages and you several lakhs (or crores). Therefore, even if your fund beats the index, does it have the best returns?

Both these funds have outperformed their index by significant margin and over the long term.

Who should invest and for how long?

PPFAS Flexi Cap is a dynamic fund with high diversification, sometimes it feels that the fund managers have tried to reduce risk of concentration so much that they have entered the territory of over diversification. This can be seen from their returns over time. This fund is a generalist and not a specialist. There is a lot of hype in the market about it and a lot of it might be hearsay, but being the flag bearer of its fund house there is a lot at stake for them to lose. The hype may be one of the reasons why it performs the way it does, as the AUM rises and fund managers run out of places to invest thus investing in stocks or sectors where they are not very confident. It is why people now call it over-saturated.

HDFC Flexi Cap and its managers are veterans of the industry; they are slow but steady. Their diversification is smaller but more accurate. They are not too far behind their biggest competitor, but that small distance can make all the difference, this means HDFC Flexi still has a lot of leeway. Perhaps in the future it may become another PPFAS Flexi but today there’s still room for more investors to board.

Both finds are best for the long-term investor. By investing for 7 years and more, the investor can assure that his funds have survived all the market ups and downs and helped them achieve their goals.